Earlier this month, we hosted our Limited Partners (LPs) for Congruent’s 2023 Annual Meeting. For the first time, we also pulled together a full day of programming for our inaugural Founders’ Summit, where Congruent portfolio companies went deep on topics ranging from board management to project finance. By putting LPs and Founders in the same room, we hoped to foster better communication, knowledge-sharing, and collaboration between these often disjointed ends of the venture ecosystem. This convening reflects our commitment to building a more cohesive and collaborative innovation ecosystem in climate.

The state of venture was a key theme this year as the rising interest rate environment, banking crisis, and tech sector headwinds have brought the soaring venture market plummeting back to earth. U.S. venture deals and dollars deployed have dropped precipitously quarter over quarter since their 2021 peak.

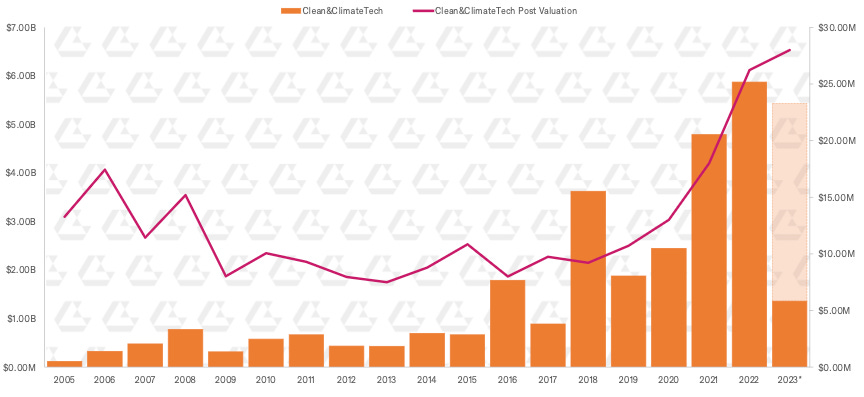

Climate, however, has proven more resilient than the broader venture market. Congruent invests early – and at our stages (Pre-Seed/Seed/Series A), climate venture continues to move along at a healthy clip.

At later stages, an IPO-starved environment and the hasty retreat of crossover funds spurred by the declining value of their public books has caused a dramatic drop in venture activity. Still, late-stage climate had a banner year in 2022 compared to every year other than 2021.

What’s going on here? While macro conditions have hammered general tech over the past year, stronger public company performance in industrials, energy, and other physical world sectors that many climate startups sell into creates a more robust customer base. Between state and federal policy, declining renewable energy costs, significant investments in electrification and decarbonization from industry, and corporate sustainability commitments, tailwinds abound for climate tech.

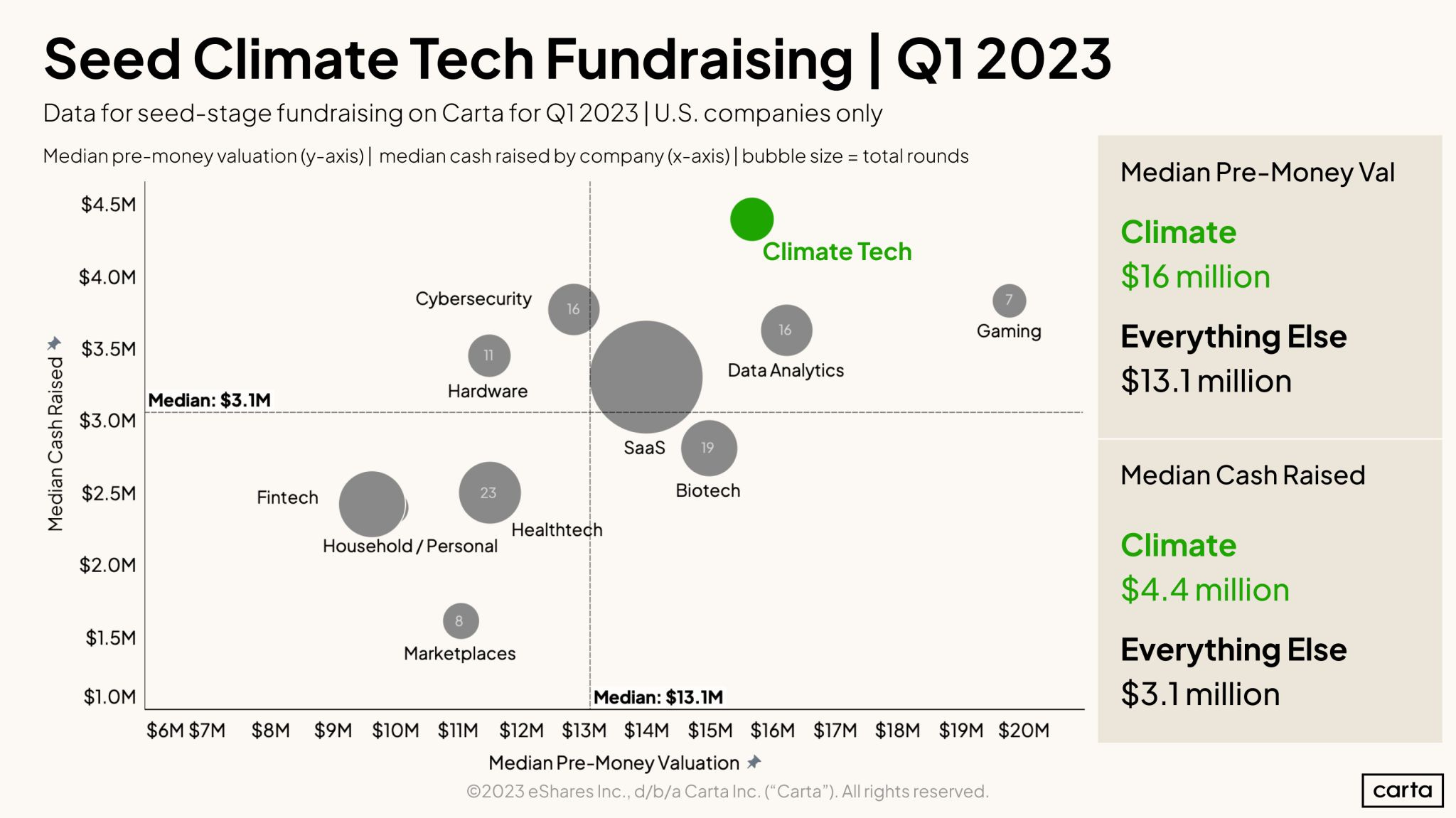

While our data sets differ, our friends at Carta tell a similar tale for early-stage climate venture in Q1 2023

The upswing of climate capital fund formation in the past couple years implies the presence of dry powder to deploy into climate companies, and while transaction volume notably declined recently (likely due to the regional banking crisis and the collapse of SVB in particular), Seed-stage climate tech companies raised larger rounds and at higher pre-money valuations compared to broader venture.

Venture will likely continue to be in flux for many quarters to come and we continue to closely monitor market conditions. We’ve included the market analysis slides that accompanied our AGM with this post. While our snapshot of climate venture activity is more conservative than most, we’re optimistic that climate venture is well-positioned to weather the storm and deliver positive both impact and returns.