Our TL;DR

Grid interconnection is not a new challenge, but the recent surge in demand – initially driven by renewable generation growth but increasingly by disproportionately large loads like AI data centers – has brought the issue to the fore. Interconnection’s central role in transmission development makes addressing its bottlenecks paramount for renewable energy deployment and grid expansion.

We’ve spoke with entrepreneurs, investors, regulators, project developers, policy experts, and technical subject matter experts to evaluate the opportunity for software to streamline the interconnection process. Based on these conversations and our research, here’s what we’re looking for:

1. Platform Functionality: Interconnection tools alone are unlikely to produce a venture outcome, but there is a much larger market opportunity for startups that can deliver value across operations. For example, integrating the interconnection process with longer-term transmission planning and process management may provide sufficient platform functionality for scale.

2. Ease of Integration & Customization: Seamless integration with existing utility tools and workflows is paramount, as are a high degree of flexibility and customization for developer-facing applications. Sales to this sector are notoriously slow and subject to startup-challenging piloting cycles. Approaches that can leapfrog this difficult pattern will be more attractive.

3. Informed Go-to-Market Strategy: Understanding of developer idiosyncrasies along with a command of utility regulatory frameworks, planning and budgetary cycles, as well as data security and privacy concerns are key to teams focused on addressing interconnection challenges.

Interconnection 101

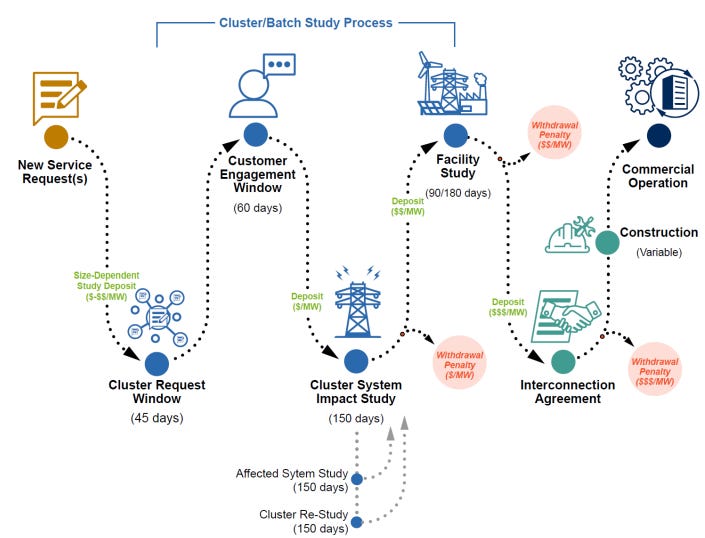

Interconnection is the process by which new generation (supply) and load (demand) resources gain access to the grid in order to draw down or feed in power. In the case of new generation, a developer submits an interconnection request to the grid operator and undergoes a series of studies that simulate each proposed project’s impact on the grid and evaluate the necessity of infrastructure upgrades to ensure grid reliability. These studies are highly technical analyses requiring significant computational resources and engineering expertise. The graphic below illustrates the key steps in connecting a generator to the bulk transmission network.

Overview of the Interconnection Process

Source: Lawrence Berkeley National Lab

Interconnection is plagued by several systemic challenges. Data is nonstandard across grid regions, quickly outdated, fragmented, and potentially subject to onerous approval processes if classified under Critical Energy/Electric Infrastructure (CEII). Information asymmetry drives developers to submit speculative projects years in advance, as queue entry becomes the primary means of obtaining reliable data. Even when accessible, data often lives in formats not conducive to discoverability or analysis; Lawrence Berkeley National Lab (LBNL) spent ~1,700 person-hours scraping PDFs to glean project-level interconnection cost estimates for their recent interconnection cost study (new tools like interconnection.fyi are directly addressing this challenge).

Technological limitations and complex cost allocation mechanisms further convolute the process. Developers bear unpredictable costs for network upgrades that could benefit the broader system, with post-construction Affected Systems Studies that evaluate impacts on neighboring grids potentially adding millions in unexpected costs. The process of identifying mitigations flagged in System Impact Studies remains largely manual, while industry standard modeling tools like PSS®E and Cyme for Power Flow, Contingency, and Stability Analyses are decades old. Analysis of electromagnetic transients (EMT) is becoming increasingly necessary as inverter-based resources (IBRs) proliferate, but existing tools (e.g. PSCAD, PowerFactory) are computationally intensive and impractical for large-scale analyses. These technical challenges are exacerbated by a shrinking workforce of power system engineers, as retirement-driven ‘brain drain’ leaves utilities resource-constrained.

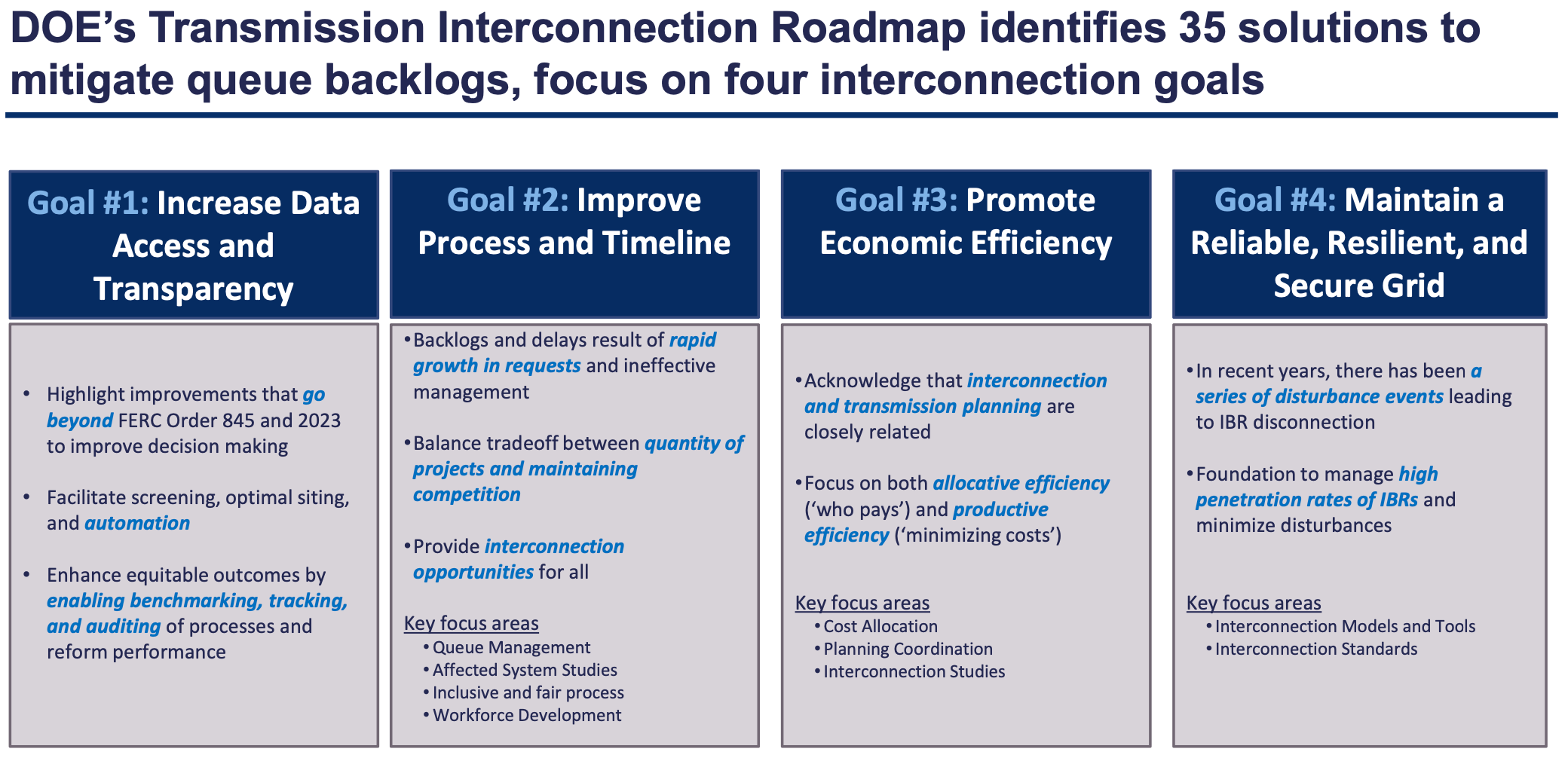

Regulators and policymakers are not blind to this problem. DOE’s i2X (Interconnection Innovation e-Exchange) program – a multi-stakeholders collaboration including utilities, regulators, developers, and researchers – published the Transmission Interconnection Roadmap in April (snapshot below) with recommendations for streamlining and accelerating the interconnection process. FERC hosted a two-day workshop on Generator Interconnection in September, convening representatives from utilities, RTOs and ISOs, academia, developers, startups, and think tanks to address needed reforms in the interconnection process and highlight potentially innovative approaches such as SPP’s proposed ‘Entry Fee’ and ERCOT’s ‘Connect-and-Manage’ approach.

Source: Department of Energy i2X

The Interconnection Problem

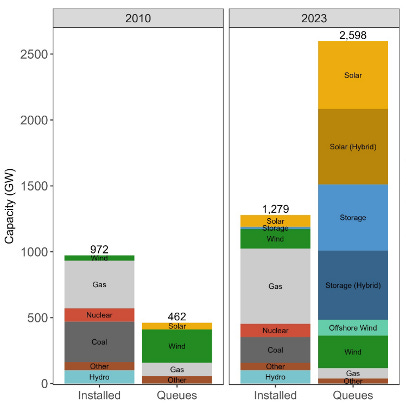

Rapid renewable development has driven significant supply-side interconnection bottlenecks over the past decade. LBNL’s latest ‘Queued Up’ report estimates there are 2.6 terawatts of generation waiting in queues – over 2x the installed capacity of the entire US generating fleet. The vast majority of that capacity is low carbon, with solar and battery storage accounting for ~80% of the 900+ GW that entered the queue in 2023.

Source: Lawrence Berkeley National Lab

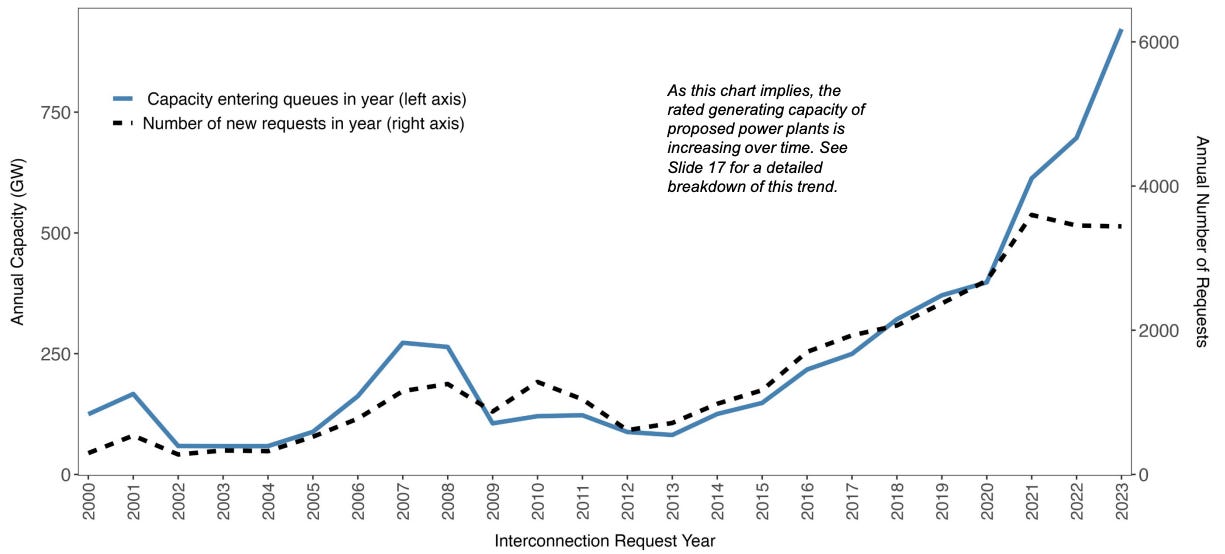

Unfortunately, most of these projects will never get built. Per LBNL, just 19% of queued projects (14% of capacity) between 2000-2018 reached Commercial Operation (COD) as of EoY 2023. Median time from interconnection request to COD has more than doubled to 5 years for projects built in 2023. Queue backlogs are so severe that CAISO (the grid operator for California) froze an entire cluster of projects from 2022-2023, while PJM (the grid operator for most of the East Coast states) froze all new requests in 2022 until at least 2026.

Source: Lawrence Berkeley National Lab

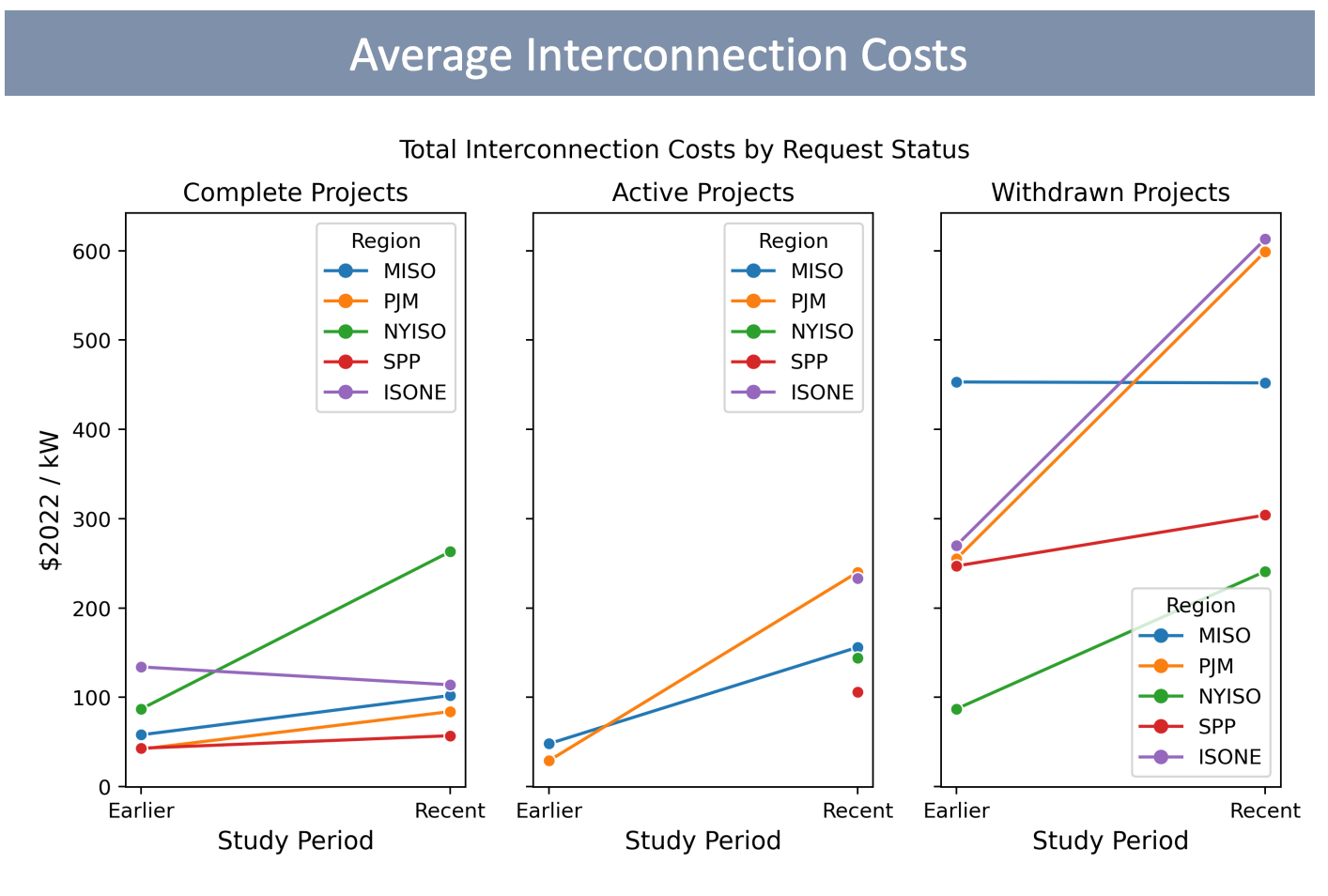

The aforementioned cost study highlights how interconnection costs have increased in all regions, driven by broader network upgrades flagged to maintain network reliability or stability. Costs for projects that have completed all studies often doubled, while active projects see even greater increases and projects withdrawn from the queue face the highest costs.

Source: Lawrence Berkeley National Lab

Longer queue times and increasing interconnection costs jeopardize project economics at a time when renewable development needs to accelerate. Despite continued growth in US clean energy deployment (~40 GW in 2024 across solar, wind, storage, and nuclear), meeting the nation’s goal of 100% carbon-free electricity by 2035 would require a near doubling of annual capacity deployments. Interconnection bottlenecks are hamstringing renewable deployment at a time when we need to put our foot on the (proverbial) gas.

A Load Growth Problem

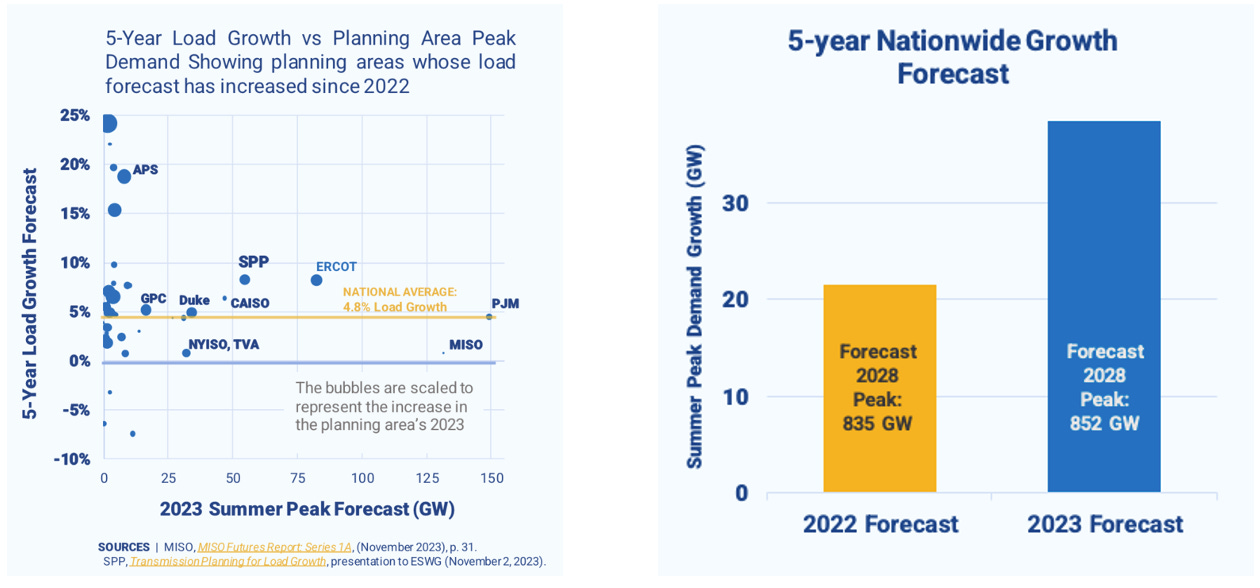

Load growth of unprecedented speed and scale complicates the picture. Last year NERC, (the North American Electric Reliability Corporation, the entity tasked with ensuring power system reliability) nearly doubled its 5-year load growth projections to 4.7%—a sea change for a slow-moving utility industry that has seen essentially zero net load growth for two decades:

Source: Grid Strategies

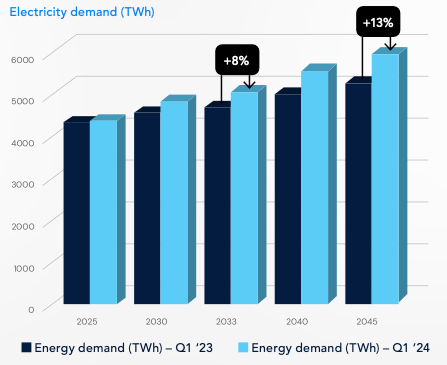

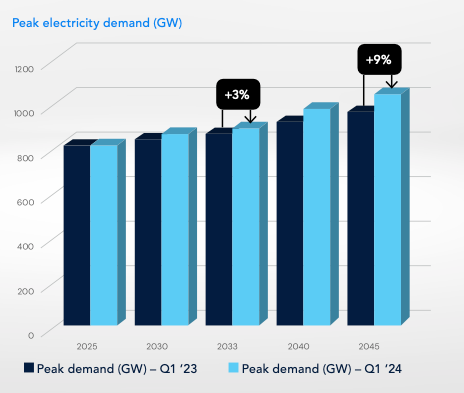

More recent estimates from ICF nearly double that again, projecting a 9% increase in national load and a 5% increase in summer peak by 2028:

Source: ICF

Massive investments in domestic manufacturing, electrification, and large-scale compute infrastructure have sent utilities scrambling. WoodMac puts it succinctly: “[the] last time the US electricity industry saw unexpected new demand growth like this was during World War II.” The disproportionate compute demands of AI data centers in particular are driving acute pockets of load growth. The GPUs required to train and run these AI models are very power hungry; AI data centers can require 3 to 5 times the power of conventional facilities of equivalent scale, with ‘hyperscale’ sites requiring hundreds of MWs if not GWs of power. Securing interconnection is the key bottleneck to data center development, and while electricity costs account for roughly 46-60% of site OpEx, hyperscalers are willing to pay a premium to secure reliable, clean power because AI data centers are such significant profit drivers. Geographic constraints and intense competition leave little flexibility in development timelines and will likely lead many groups to bypass the interconnection logjam by pursuing behind-the-meter solutions. Amazon and Talen Energy are revising a planned expansion of power sales from the Susquehanna nuclear plant in Pennsylvania to a co-located AWS data center after FERC recently rejected their proposal due to concerns of undue impact on ratepayers. Google plans to contract for 115MW from Congruent portfolio company Fervo Energy via NV Energy, and Microsoft signed a 20-year PPA with Constellation Energy to restart Unit 1 at 3 Mile Island and purchase 100% of that reactor’s output. All three have invested in – if not already contracted power – from early-stage nuclear fusion or small modular fission reactor companies.

Transmission planning teams at 9 of the country’s 10 largest utilities cited data centers as a main driver of load growth in earnings calls earlier this year – up from just 2 during the same period last year. Dominion Energy (the utility for VA and NC) is regularly getting asked to interconnect loads of several gigawatts against a generating base of 34 GW. Our grid is physically unprepared to accommodate this influx of demand due to lagging transmission development, and grid operators are logistically unprepared to manage it given their long planning cycles and resource constraints. Most don’t even have formal process for interconnecting large loads given historically tepid demand growth.

A Failure of Transmission Planning

These challenges compound to constrain transmission development at a time of needed acceleration. DOE’s National Transmission Needs Study estimates a nationwide buildout of 54,500 GW-mi is required to meet “future scenarios with moderate load but high clean energy assumptions” (i.e. as enabled by the current policies like the IIJA and IRA). This translates to a ~64% expansion of the transmission system as of 2023. The annual growth rate of transmission over the last decade has been around 1% per year, with average deployment of 2,000 miles from 2012-2016 decreasing to just 700 miles from 2017- 2021. Just 55 miles of new high-voltage transmission were built in 2023. Despite the lack of new capacity, reliability upgrades and replacement of aging infrastructure drove to annual transmission expenditures to a record $25+ billion last year.

Lack of proactive, coordinated transmission planning has resulted in interconnection requests being a primary driver of transmission development and led to the patchwork grid we have today. Regulators have recognized these challenges but continue to promulgate incremental, piecemeal reforms. Last November’s FERC Order 2023 mandated cluster-based queue processing along with stricter penalties on both developers and grid operators to improve efficiency and disincentivize speculation but fell short of addressing cost allocation or granting FERC backstop authority for siting critical projects. Order 1920 from this May enhanced transmission planning by requiring improved coordination and the adoption of advanced modeling techniques to better address emerging grid challenges. It updated the long-term planning time frame to 20 years, encouraging utilities to incorporate renewable resources and future grid needs more proactively, but stopped short of mandating regional coordination or addressing cost allocation for large-scale transmission projects. Pressure is mounting on FERC to overhaul both the interconnection and transmission planning processes, but policy experts do not expect another major ruling on interconnection anytime soon.

This regulatory and technical morass leaves climate investors with a unique conundrum: many infrastructure projects are now bottlenecked by power needs, and the path to popping the proverbial cork is not clear. So how does an entrepreneur or investor address this problem? Congruent does not have the answer, but we are interested in innovative solutions that can address a meaningful slice of this system-wide challenge.

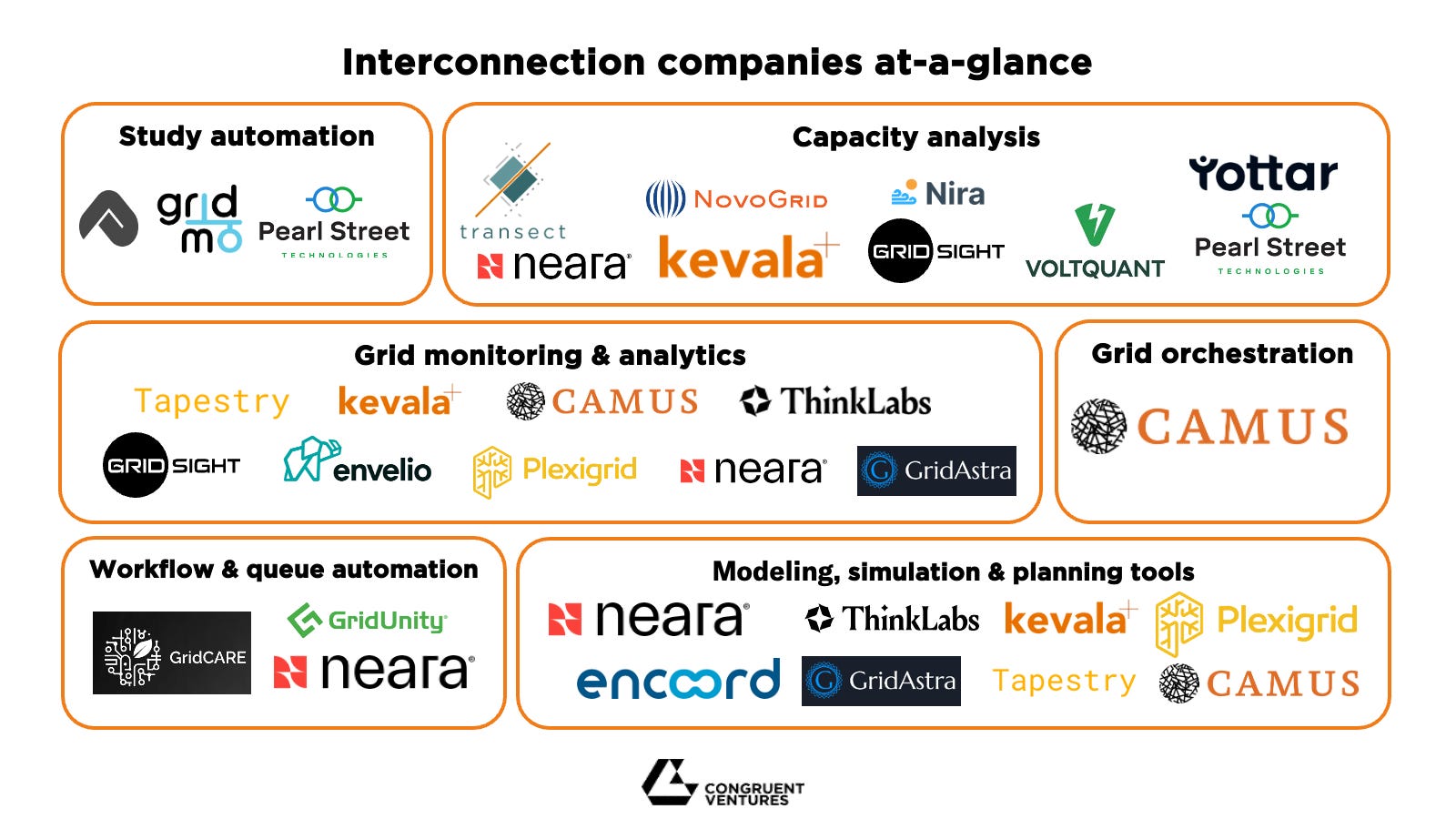

The Interconnection Innovation Landscape

Congruent invests in bits, atoms, and everything in between. Digital solutions can accelerate and optimize the deployment of physical solutions such as Advanced Conductors (shoutout to Congruent portfolio company VEIR), Dynamic Line Rating, Topology Optimization, and other Grid-Enhancing Technologies. Many startups are addressing interconnection, but few have made it their entire business. There is significant functional overlap across grid software applications, making distinct characterization challenging. The list below is not intended to be exhaustive – please reach out if we missed your company!

Congruent’s Bull & Bear Perspectives

Enablers (Bull View):

- Transmission Constraints: Significant growth in transmission capacity is required to meet the needs of an increasingly renewable and distributed grid and ensure system reliability. Rapid and acute load growth coupled with the increasing penetration of non-dispatchable resources on a transmission-constrained grid is making Resource Adequacy a real concern during utility scenario planning. Software solutions that streamline the interconnection process can meaningfully accelerate grid expansion because interconnection is such a significant driver of transmission.

- Technology & Process Gaps: Interconnection is dominated by legacy tools from incumbent software providers. Persistent analog and manual processes limit coordination as well as data availability and quality. Modern software tools leveraging the latest advances in computational techniques, data management, cloud computing, and AI/ML can drive significant process efficiencies across applications.

- Regulatory Pressure: FERC, DOE, and state-level actors are applying tangible pressure on grid operators to streamline the interconnection process and integrate emerging technologies. We believe there is an opportunity for startups to fill this technology gap.

Obstacles (Bear View):

- Adoption Cycles: There are inherent challenges to scaling startups in this space. Utilities’ and grid operators’ reliability mandate makes them risk-averse and slow adopters of new technologies, while developers are more commercial but constitute a smaller market opportunity and tend to be idiosyncratic.

- Regulatory Risk: Interconnection challenges are symptomatic of broader dysfunction in grid planning. Recent FERC orders and ISO/RTO-level reforms, while slow-moving and incremental, signal willingness to address these challenges head-on. A regulatory overhaul could diminish the value proposition of interconnection startups by obviating the process inefficiencies they are addressing.

- Limited Opportunity Size: This space is highly intermediated by consultants and entrenched legacy software providers. With few public or sizeable M&A comps to benchmark against, it is unclear there is potential for a large outcome for a startup building in interconnection.

Focus areas

A quick policy detour: the outgoing Biden administration recently published a memorandum calling for interagency coordination to “streamline permitting, approvals, and incentives for the construction of AI-enabling infrastructure,” including transmission. Just yesterday, DOE announced $30M in funding from the Bipartisan Infrastructure Law for solutions that leverage artificial intelligence to accelerate the interconnection process. Although the incoming Trump administration’s stance on transmission is unclear, grid expansion and power system reliability are bipartisan issues. Congruent is actively tracking the ‘GRID Power Act’ (H.R. 9801), Congressman Troy Balderson’s (R-OH) bill directing FERC to initiate a rulemaking requiring that transmission providers prioritize new dispatchable generation in interconnection queues. While the fate of Sens. Joe Manchin’s (I-WV) and John Barrasso’s (R-WY) ‘Energy Permitting Reform Act of 2024’ (S.4753), is uncertain, a unified Republican government will almost certainly pursue permitting reform by weakening regulations such as NEPA along with EPA rules and other perceived forms of red tape. It is too early to gauge whether the administration will pursue a technology-agnostic stance or seek to penalize renewables in favor of fossil energy development. As for FERC, president-elect Trump can nominate a new chairperson on day one, but the five-member Commission still proceeds by vote and could maintain its existing Democratic majority for another 18 months given its rolling terms and the spate of recent appointments.

While we are concerned about the net environmental impacts of rolling back environmental regulations, we are cautiously optimistic that a second Trump term may result in a more favorable permitting regime for transmission and other critical infrastructure, and will continue to update our thinking as the new administration takes shape.

There is no clear roadmap for selling software to utilities, developers, or grid operators, and few examples exist of startups that have successfully scaled in those segments. Congruent invests in companies we believe can grow rapidly to capture a large market opportunity and generate outsized returns on both capital and impact. We have identified at least four discrete critical technology gaps that could be filled by a software startup, but ultimately believe value will accrue to platforms that can integrate several functions and sit across multiple utility/grid-operator business units:

- Data Layers: Utility or grid operator-maintained platforms that provide transparent, real-time grid information to developers such as queue status and location-based availability of injection/withdrawal capacity. AEMO’s Connection Simulations Tool is a prime example and allows registered participants to run their own analyses using the grid operator’s full power system model.

- Advanced Grid Modeling Tools: Automation of complex grid studies like contingency and dynamic stability analyses offers a significant opportunity to reduce interconnection timelines and improve reliability. EMT tools capable of larger, system-wide analysis in a computationally efficient manner are needed as IBRs make grid behavior increasingly complex.

- Workflow Automation: Streamlining the highly manual and cumbersome queue management processes will be essential to reducing project delays and speeding up interconnection timelines. Everything from application management to communication of timelines and costs with developers.

- Data Center Performance Improvement: given the extreme power needs of AI data centers, we expect to see innovation focused on behind the meter power usage effectiveness (PUE) in many forms to maximize compute output within the fixed load footprint.

Please reach out if you are building in any of these areas. With the exception of Camus Energy, we have not yet made an investment directly in this category, and we look forward to meeting entrepreneurs tackling these challenges head on!

Sources

1. Lawrence Berkeley National Lab (1)

2. Lawrence Berkeley National Lab (2)

3. DOE Interconnection Innovation E-Exchange

4. DOE I2X Transmission Interconnection Roadmap

5. FERC Generator Interconnection Workshop

6. Lawrence Berkeley National Lab (1)

7. Lawrence Berkeley National Lab (2)

10. ICF

11. WoodMac

12. IDC

13. Utility Dive (1)

14. Bloomberg

16. New York Times

17. Reuters

18. DOE Grid Deployment Office

19. Utility Dive (2)

22. Ibid

23. FERC

24. FERC(2)

26. Whitehouse.gov

27. DOE Grid Deployment Office

28. Congress.gov

29. Senate Committee on Energy and Natural Resources

30. The Hill

31. Utility Dive (3)